Global subsea engineering, procurement and construction (EPC) awards totaled approximately US$17 billion for 2025, a 20% year-on-year decline, but Guyana remained one of the few bright spots as major projects advanced, according to Westwood Energy Global Group.

In an analysis published on January 21, Westwood said the lower award value came despite 53 final investment decisions (FIDs), around 230 subsea tree units, about 2,200 km of subsea umbilicals, risers and flowlines, and roughly 1,560 km of pipeline being sanctioned worldwide.

Westwood attributed the slowdown to “lower-than-expected oil prices and high supply chain costs,” which “negatively impacted E&P’s investment appetite”. The subsea EPC cost index still rose about 25% compared with a 2021 baseline, though it was 14% lower than in 2024, showing easing cost pressure late in the year.

The analysis noted that average oil prices in 2025 fell 20% from the 2021–2022 average of US$85.9 per barrel, putting pressure on free cash flow and driving “a renewed focus on cost efficiency across the value chain”. This prompted timeline revisions for projects offshore Mexico and Malaysia as operators cited “high supply chain costs and the need for project optimisation”.

Against this backdrop, Guyana featured prominently among the few countries sanctioning large subsea developments requiring floating production systems. Westwood pointed to the Hammerhead development by ExxonMobil as one of the major projects approved in 2025, alongside developments in the U.S. Gulf, Brazil and Mozambique.

Westwood said the supply chain is now under pressure to deliver cost reductions of “approximately 15–20%” from the 2024 subsea EPC cost index, a level it described as “essential” given expectations of a “persistently oversupplied oil market”. Global oversupply is forecast to reach about three million barrels per day in the first quarter of 2026, the highest since 2020.

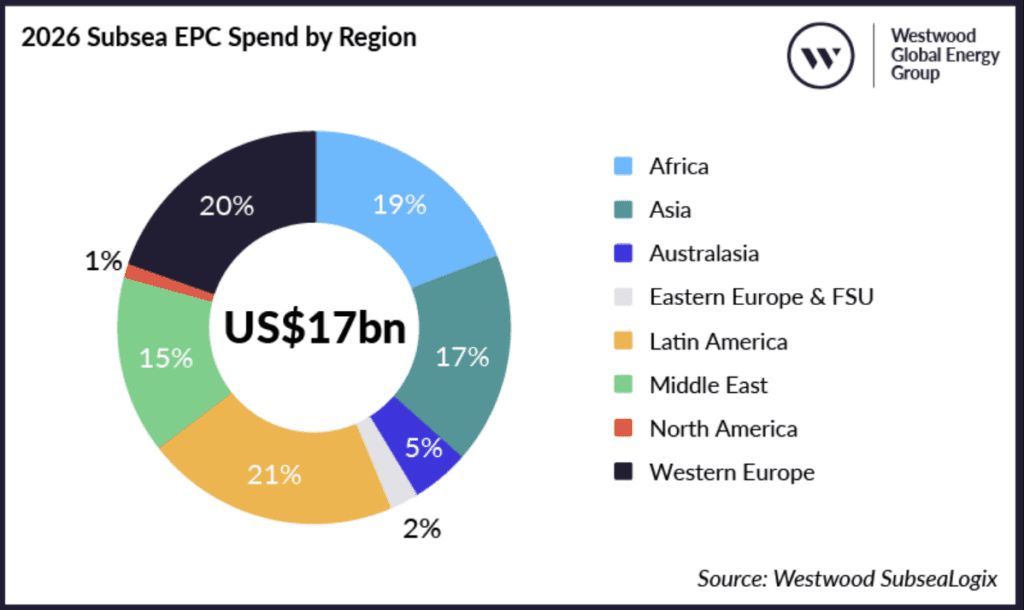

Looking ahead, Westwood expects subsea EPC spend in 2026 to remain around US$17 billion, like 2025 levels, even as field FIDs could rise 13% year-on-year to about 60. It said unit costs are projected to continue trending downward, as seen since the second half of 2025, supporting planned investments.

Over the 2026–2030 period, Westwood forecasts up to US$90 billion in subsea EPC contracting opportunities, with demand for about 1,300 subsea trees. Within this outlook, Guyana is expected to remain active, with ExxonMobil’s offshore portfolio set to expand further through the sanctioning of the Longtail development.

{kind=link}