2020 was a difficult year for the world’s refineries as the coronavirus pandemic reduced refinery utilisation and OPEC+ supply restraint narrowed crude price differentials. Despite this, integrated refinery and petrochemical sites significantly outperformed their fuels-only peers, according to Wood Mackenzie.

One of the most highly integrated sites in China, Hengli, generated a net income of more than US$1.4 billion during Q1 to Q3 2020, at a time when most of the refining industry was incurring significant losses.

Alan Gelder, Wood Mackenzie VP Refining, Chemicals & Oil Markets, said: “Over the coming years, the energy transition and the associated electrification of the passenger car fleet will slow the pace of global gasoline demand growth and drive it into decline after 2030.

“Meanwhile the versatility and durability of petrochemicals will see sustained demand growth, particularly in the developing economies of Asia, with global petrochemical feedstock demand growing by over 500,000 b/d each year over the next decade. This growth in petrochemical feedstocks will be tempered by an increase in global recycling rates as societies focus on reducing the environmental challenges of plastic waste.

“This switch in demand away from gasoline to petrochemicals promotes the adoption of refinery and petrochemical integration, particularly for new facilities in Asia and the Middle East. Currently, more than 30% of the world’s refineries are now integrated with commodity petrochemicals. These sites benefit from both a diversified product slate, and the potential to unlock greater value through economies of scale and operational cost synergies.

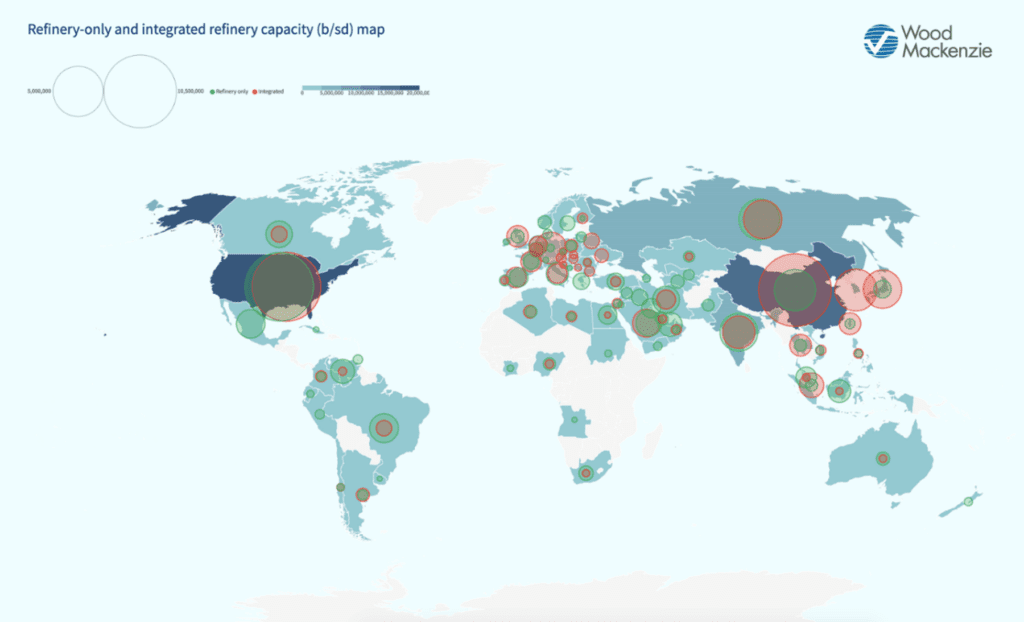

China has already outlined an integrated refinery and petrochemicals path that achieves earnings comparable with the most profitable refining sites in North America, says Wood Mackenzie.

Two second-generation integrated sites, Hengli and RhongSheng, were brought online in 2019 and achieved full operations in 2020. Had they been fully operational in 2019, they would have been among the world’s top performing sites for 2020 when measured in earnings per barrel of crude processed, estimated at around US$10/bbl, according to Wood Mackenzie’s REM-Chemicals tool.

“The development of these sites and fast followers is to be closed watched as their deployment has global consequences. The new integrated sites in China are achieving a chemical yield of over 40wt%. The development of such highly competitive sites makes it increasingly difficult for refineries in the Atlantic Basin to export their surplus gasoline, so the further growth of such sites will accelerate refinery closures in Europe and the US.

“Though China is currently a runaway leader in the integrated refinery and petrochemicals space, India’s significance as an investment location is expected to rise over the coming years. The Middle East has invested in expert refining and has recently become more interested in integration as a means of adding value to its crude exports because its supplies of gas-based feedstocks are dwindling,” added Gelder.

{kind=link}