As COVID-19 infections continue to increase around the world and the implications of the pandemic’s spread are acknowledged in key markets in the Americas and Asia, Rystad Energy is now changing its base case scenario for oil demand, incorporating a mild second wave effect.

The updated base case scenario assumes a temporary pause in global demand recovery, as the reopening of Europe and other regions is offset by COVID-19 outbursts in populous and high oil-consuming countries in the Americas and Asia such as the United States, Brazil and India, among others.

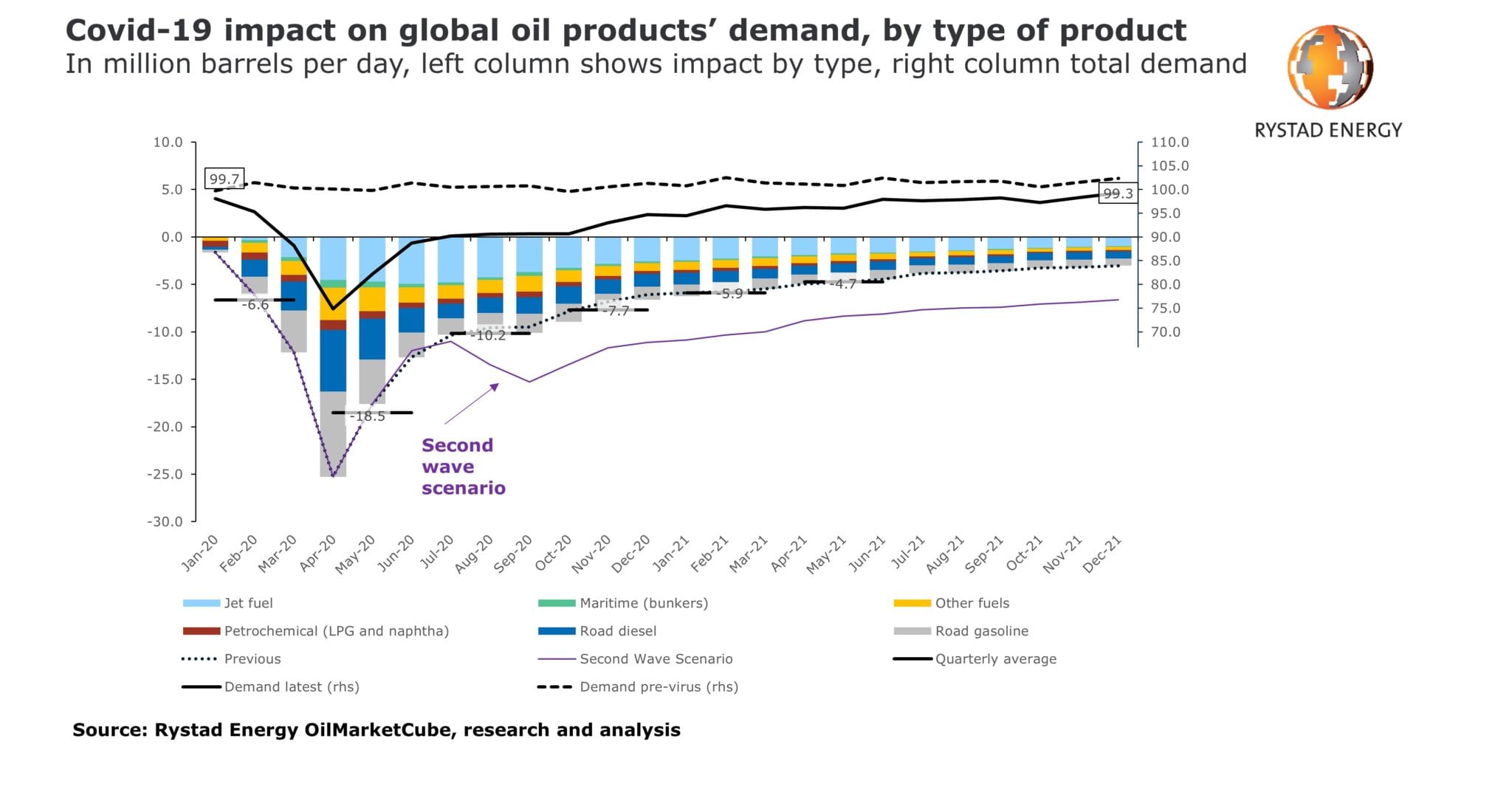

“There is downside risk to our base case. We have identified a category of oil demand at risk – that is, the maximum number of barrels that could be lost if a full lockdown is reinstated globally. In this worst-case scenario in which strict lockdown measures return, we expect demand to edge around 3.7 million bpd lower for the rest of 2020, compared to our updated base case scenario,” Rystad Energy said in its report published on Friday.

Even if the disease is not reigned in and this full-blown second wave manifests, Rystad Energy said the effect on oil demand will not be as destructive as during the first shock in April 2020. That is because the world is better prepared to introduce smarter and more targeted lockdowns, handle infections, and also because the global economy can simply not afford another steep economic meltdown.

In this update, instead of gradually recovering monthly, Rystad Energy said global oil demand in its base case is now expected to stay relatively flat from July to October 2020 and then inch up again from November, albeit at a much slower rate than previously estimated. In July, oil demand is now expected to average 90.2 million barrels per day (bpd) and then improve to an average of 90.6 million bpd for August, September and October. In November, oil demand is likely to reach 93 million bpd and in December climb a bit more to 94.7 million bpd – still a far cry compared to the pre-COVID oil demand average level of more than 99 million bpd in 2019.

The mild second wave is expected to last into January and February 2021. Rystad Energy said from March 2021 onwards, its updated base case scenario does not diverge from its previous base case that did not incorporate a second wave.

On an annualized level, the updated base case scenario shows global oil demand is now forecast to reach 89.7 million bpd in 2020 and 97.1 million bpd in 2021.

“We do not expect full demand recovery in 2021 as structural growth drivers are still not set to snap back. Furthermore, some fuels remain marginally depressed, with aviation activity not fully recovering before the end of 2022, when, in the best case, oil demand will approach pre-virus levels,” says Rystad Energy’s senior oil markets analyst Artyom Tchen.

The halt in demand recovery in its updated base case scenario is predominantly due to a slowdown in road fuel demand from August, which otherwise enjoyed a big boost in July.

“While in June road diesel landed 2.57 million bpd lower than our pre- COVID-19 estimates, it picked up in July and will lag only by 1.56 million bpd,” Rystad Energy said. Similarly, road gasoline landed 2.61 million bpd lower than our pre-pandemic estimate in June and will only trail by 1.71 million bpd in July. From next month though, Rystad Energy’s current base case shows that this demand gap against its pre-virus estimates will widen again.

The above gap for diesel will reach 1.63 million bpd in August, 1.73 million bpd in September and 1.82 million bpd in October, before shrinking to 1.49 million bpd in November and 1.34 million bpd in December this year. For gasoline, the gap will reach 2.04 million bpd in August, 2.01 million bpd in September and 1.92 million bpd in October, before closing to 1.57 million bpd in November and 1.40 million bpd in December.

Rystad Energy said it is worth noting that jet fuel is not expected to follow a similar path, as airlines have implemented strict measures and are slowly but steadily restarting disrupted flight routes, providing some summer transport relief for healthy passengers.

“The gap between the current demand estimate and our pre- COVID-19 projection for jet fuel reached 4.94 million bpd in June, will land at 4.77 million bpd in July and will be shrinking for every single month until the end of 2020, according to our updated scenario,” Rystad Energy stated. “That said, jet fuel is the fuel currently most hit by the pandemic and, as mentioned earlier, it will take a much longer period to fully recover.”

In the grim case of the full-blown second wave lasting from Aug-20 to Oct-20, there will be long-lasting demand impacts that carry into 2021 and beyond, Rystad Energy said.

{kind=link}