The Natural Resource Fund Act 2021

Summary

- The Natural Resource Fund Act 2021 did not propose the removal of any component from the 2019 Act per se, rather, the bill seeks to replace certain components in the current act that conforms to international best practices – following the Santiago Principles.

- The ultimate oversight body of the fund is the National Assembly, the Public Accounts Committee, the Bank of Guyana, the Board of Directors, the Public Accountability and Oversight Committee which by design will exercise non-governmental oversight, and the Ministry of Finance.

- With respect to transparency and accountability, the bill mandates monthly, quarterly, and annual reporting. The annual report has to be tabled in the National Assembly, and the Fund is subject to both internal and external audit.

- The Board has management responsibility of the fund, and, the Board has to be guided by the legislation on how the fund ought to be managed. The Board, therefore, cannot (legally) deviate from the investment mandate of the fund as stipulated by the Act.

- The Act is inclusionary of all key stakeholders in national development, particularly, civil society groups, women representation, the private sector, the Political Opposition, professional associations, and labour representation.

Background

The Natural Resource Fund Act 2019 is an important piece of legislation albeit–for reasons of constitutional legitimacy, transparency, accountability, and governance of the Fund, the 2019 Act is set to be amended, inter alia, the Natural Resource Fund Bill 2021. This position was made clear by the current Administration when in Opposition. Hence, the premise of this bill is a commitment being honored by the government of the day.

Discussion and Analysis

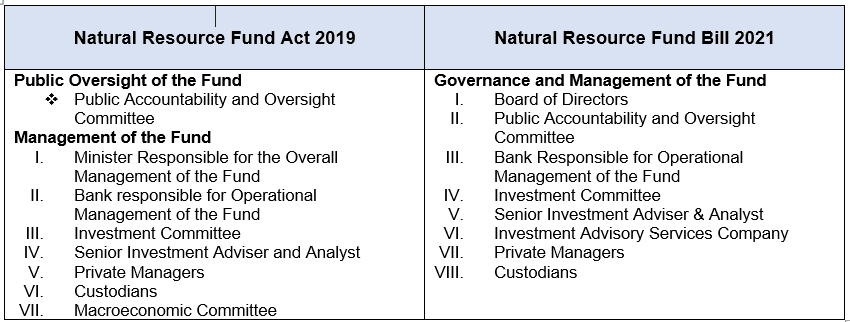

Comparison of the Natural Resource Fund Act 2019 and the Proposed Amendments in the 2021 Bill: Key Components

The notion that the Public Accountability and Oversight Committee is being removed in the proposed Amendments is grossly inaccurate. The amended bill in fact seeks to recalibrate the Committee in such a manner that the Committee can function effectively and efficiently for all practical reasons. In so doing, the twenty-two-member committee has been reduced to nine as follows:

- One nominee of the National Assembly;

- Three representatives from the religious community;

- Two representatives of the private sector;

- Two representatives of the organized labour; and

- One representative of the professions

It is noteworthy to point out that in the recalibrated structure of the said Committee, (1) instead of having the one nominee each from the ten Administrative Regions, the ten Administrative Regions can be represented by one nominee from the National Assembly and that nominee, perhaps may require at least a two-third majority support in the National Assembly; (2) instead of having one member each from the various professional associations such as the accounting profession, the legal profession, the journalists etc., in the new structure, all the professional associations would have to come together through a consultative approach to nominate one representative to represent all of the professional associations; (3) where in the current Act there is one nominee from a number of different civil-society groups – these groups need to now come together through a consultative approach and nominate three representatives to represent all of those organizations.

In a similar manner, the two representatives from the private sector would have to be nominated to represent all of the private sector associations across the country and the same goes for the labour representative. Thus, the burden for all these named stakeholder groups, organizations and associations now rests on their shoulders to agree on a single nominee, in one case two and in another three, to represent all of their interests on the Committee.

Notably, the above illustration has demonstrated that the Public Accountability and Oversight Committee has not been removed as has been falsely propagated by some sections of the media, and the wide cross section of representation from the private sector, civil society groups, labour unions and the professional associations has not been diminished in the recalibrated structure of the Committee.

The 2019 Act confers the full management responsibility upon the Minister of Finance, which by all standard, is a deviation from the Santiago Principles and constitute a great degree of political domination which can effectively compromise transparency, accountability, and good governance of the Fund. This element has been replaced by a Board of Directors comprising a minimum of three members and maximum of five members appointed by the President. The Bill speaks to the qualifications and experience of the Directors and that one of whom shall be nominated by the National Assembly, and one from the private sector.

Though the bill did not elaborate on the procedure on how all of the Directors are to be nominated and appointed, the bill did empower the Minister of Finance to make regulations wherein “…generally for the better carrying out of the purposes of this Act taking into account the generally accepted principles and practices on sovereign wealth funds as contained in the Santiago Principles.”

Compliance with the Santiago Principles

The Santiago Principles is a voluntary set of twenty-four guidelines designed to promote good governance, accountability, transparency, and prudent investment practices as well as maintain a stable and open investment climate. The Santiago Principles are now observed by more than twenty countries’ Sovereign Wealth Funds (SWFs).

The implementation of these principles can be grouped into three key areas:

- Legal framework, objectives, and coordination with macroeconomic policies: in the case of Guyana, the legal framework is the legislation, namely, the Natural Resource Fund Act. The Objectives of the Fund is set out in the Act and those objectives are aligned with the economic policy and development agenda of the government of the day.

- Institutional framework and governance structure: the institutional framework in the case of Guyana is the operationalization of the Fund, which is held in the Federal Reserve Bank, the Bank of Guyana which has responsibility for the operational Management of the Fund, the Board of Directors, the Public Accountability and Oversight Committee, the Ministry of Finance, and then ultimately, the National Assembly.

- Investment and risk management framework: in the case of Guyana, this is the investment committee, the investment adviser (s), the private manager (s), and the investment advisory company.

The 2019 Act conferred the full management responsibility upon the Minister of Finance, which by all standard, is a deviation from the Santiago Principles and constitute a great degree of political domination which can effectively compromise transparency, accountability, and good governance of the Fund. This element has been replaced by a Board of Directors comprising a minimum of three members and maximum of five members appointed by the President.

The Act speaks to the qualifications and experience of the Directors and that one of whom shall be nominated by the National Assembly, and one from the private sector.

Though the Act did not elaborate on the procedure on how all of the Directors are to be nominated and appointed, the Act empowers the Minister of Finance to make regulations wherein “…generally for the better carrying out of the purposes of this Act taking into account the generally accepted principles and practices on sovereign wealth funds as contained in the Santiago Principles.”

The overarching framework for the nomination and appointment of members and directors on the various committees is also set out in the Act.

The Act removed the Macroeconomic Committee which in the 2019 Act is the Committee that is appointed by the Minister of Finance that advises the Minister on the (previously) fiscally sustainable sum. Be that as it may, the macroeconomic committee was removed because it is not necessary at this point in time given that there is such a committee already in place at the Ministry of Finance. Therefore, this would have been duplication of work.

Withdrawal from the Fund

All withdrawals from the fund have to be deposited into the Consolidated Fund in accordance with the Act, thus, subjecting the monies from the fund to full parliamentary scrutiny and approval through the budget process.

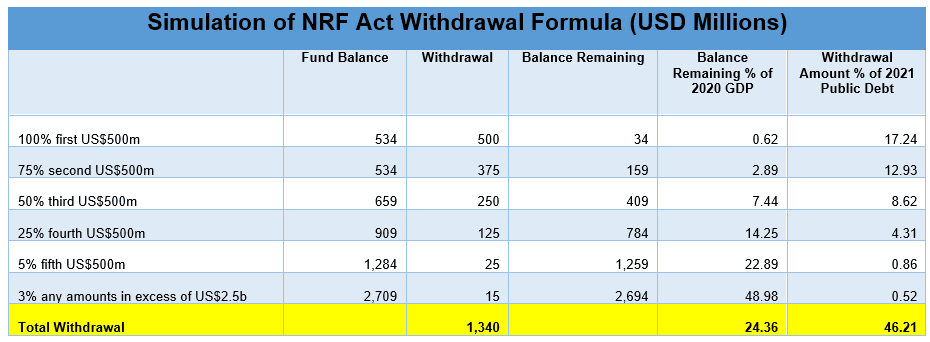

According to the withdrawal rules (first Schedule), the ceiling on annual withdrawals are as follows:

- 100% of the first US$500 million

- 75% of the second US$500 million

- 50% of the third US$500 million

- 25% of the fourth US$500 million

- 5% of the fifth US$500 million

- 3% of any amounts in excess of US$2.5 billion.

With this simplified formula, one can observe that the withdrawal rules of the fund are NOT designed to withdraw all the monies from the fund especially as the balance in the fund starts to grow. The upfront drawdown from the fund is necessary to kickstart and advance Guyana’s massive development agenda in infrastructure (new roads and bridges, irrigation, social infrastructure, health care, education, national security, and ICT etc.) all aimed to modernize and transform the economy and diversify the economy away from oil and gas. This is in keeping with a sustainable development model thus preventing the economy from being exposed to any significant risks of bankruptcy and external shocks.

There is another important positive impact as a direct result of this withdrawal model as well and that is, the reduction in the national debt in the first five years at least thereby freeing up more liquidity in the banking sector to the private sector. As such, this auger well for the long-term macroeconomic stability framework of the economy as the country seeks to accelerate development to a modern economy. In other words, what might take 50 years to achieve without oil, we can now achieve in 25 years or half that time.

Important to note as well that the investments of today are also for the benefit of the future generation and the present generation. The new four-lane roads that will be built, the education system, cheaper energy, etc., will be enjoyed by the present and future generation.

The above table demonstrates the application of the withdrawal formula for the Natural Resource Fund in accordance with the Natural Resource Fund Act 2021.

The notion that the withdrawal rules are designed deplete the fund is inaccurate.

As demonstrated above:

- 100% of the first US$500m will leave a balance of US$34m in the fund

- 75% of the second US$500m will leave a balance of US$159m

- 50% of the third US$500m will leave a balance of $409m

- 25% of the fourth US$500m will leave a balance of $784m

- 5% of the fifth US$500m will leave a balance of US$1.2b

We cannot only save for the future generation, we have to invest in the facilities, infrastructure, education system etc., today, for the future generation to enjoy.

Conclusion

Altogether, the Natural Resource Fund Act 2021 did not remove of any critical component from the 2019 Act per se, rather, the bill seeks to replace certain components in the current act with those that align with international best practices – following the Santiago Principles. Ultimately, the aim is to ensure greater accountability, transparency, and prudent governance of the fund in the interest of the people of Guyana.

The ultimate oversight body of the fund is the National Assembly, the Public Accounts Committee, the Bank, presumably the Central Bank/Bank of Guyana, the Board of Directors, the Public Accountability and Oversight Committee which by design will exercise non-governmental oversight, and the Ministry of Finance.

With respect to transparency and accountability, the Act mandates monthly, quarterly, and annual reporting. The annual report has to be tabled in the National Assembly, and the Fund is subject to both internal and external audit.

Further, the management of the fund is not to be determined by the Board per se, rather the Board has management responsibility of the Fund, and, the Board has to be guided by the legislation on how the Fund ought to be managed. The Board, therefore, cannot (legally) deviate from the investment mandate of the Fund as stipulated by the Act.

With regards to the appointment of the Board, it is normal practice in other countries that the Board be appointed by the President. While the legislation did not speak to the procedure on how the Board will be appointed, the bill did empower the Minister to make regulations to aid the implementation of that which will be enshrined in the Act.

The 2021 Act is in line with a more prudent structure from a transparency and accountability perspective as well as a governance standpoint.

Irrespective of who appoints the Board and who comprised the Board and the other committees such as the Investment Committee, those persons cannot act on their own accord or upon the directive by the President per se or any political party. Rather, those persons ought to execute their functions in accordance with the legal parameters as set out in the Act regarding the investment mandate and overall management of the fund.

The overarching framework for the investment committee, the withdrawal rules as well as the functions of those committee and the Board are clearly set out in the Act and therefore any deviation will be in contravention of the Act. And of course, in any such instance, there will be legal consequences for breaches of the Act, if for example, there is misappropriation of funds, the penalties that are stipulated in the Fiscal Management and Accountability Act will be applicable.

Finally, the NRF Act is good for Guyana and effectively paves the way to advance the prosperity of all the people and enhancing the quality of life for every Guyanese.

About the Author

Joel Bhagwandin is a Financial Analyst and has been providing insights and in-depth analyses on national cross cutting issues surrounding public policy, economic and finance issues for the past 5+ years on a variety of thematic areas within this sphere. The views, thoughts and opinions expressed in this article belong solely to the author, and not necessarily to the author’s employer, organization, committee, or other group or individual. The author is the holder of a master’s degree in banking & finance and he is [currently] undertaking four professional certifications in Corporate Finance through the Corporate Finance Institute (i.e., the FMVA, CBCA, CMSA & BIDA professional designations).

{kind=link}