The crude oil market is staring into an abyss. The challenges are physical – dealing with extreme oversupply – and financial, with market participants from wellhead to forecourt under severe duress. Ann-Louise Hittle and Alan Gelder, who, respectively, lead Wood Mackenzie’s oil market and downstream analysis, provide some insight in the latest edition of The Edge.

Demand is collapsing

WoodMac said its Macro Oils service forecasts global liquids demand will drop by 8.1 million b/d on average to 90 million b/d in Q2 2020 year-on-year, and a meaty 10 million b/d from the all-time peak of 100 million b/d in Q3 2019. This represents an unprecedented drop.

The UK-based consultancy group said the averages don’t begin to tell the whole story – the downward pressure on demand is likely to be more severe in the next few weeks as containment measures peak. Chinese oil demand fell by 19% year-on-year in Q1; but the February fall at peak COVID-19 was 35%. In Q2, other big oil-consuming economies in Europe and the US will feel the full effect of the lockdown on gasoline and jet fuel in particular. At times during Q2, global demand could drop by more than 10 million b/d, depending on how the lockdowns progress.

Supply still rising – for the moment

WoodMac said Saudi Arabia sprung from the debris of the OPEC+ disintegration in early March, determined to increase market share. The Saudis plan to add over 2 million b/d, taking sales to 12.3 million b/d in April, with volumes from storage topping up production.

Saudi Arabia is offering its crude at steep discounts to secure sales, with varying degrees of success. It’s a shock-and-awe tactic that’s driven prices down. The ulterior motive is to gain market share, including in Europe where Saudi Arabia competes with Russian oil. Russia, also free of OPEC+ constraints, has the potential to increase production by up to 0.4 million b/d – but it is not yet clear if they will significantly ramp-up supply. Brent dropped 60% to below US$25/bbl in three weeks.

Little or no volumes have yet shut down in response to the fall in price. WoodMac estimates that 10 million b/d of global production is below short-run marginal cost (SRMC) at US$25/bbl Brent, but producers typically adopt a wait-and-see approach because of associated shut-in costs. It’s only a matter of time – barring an about-turn by the Saudis and Russia perhaps under pressure from President Trump.

Where will the surplus oil go?

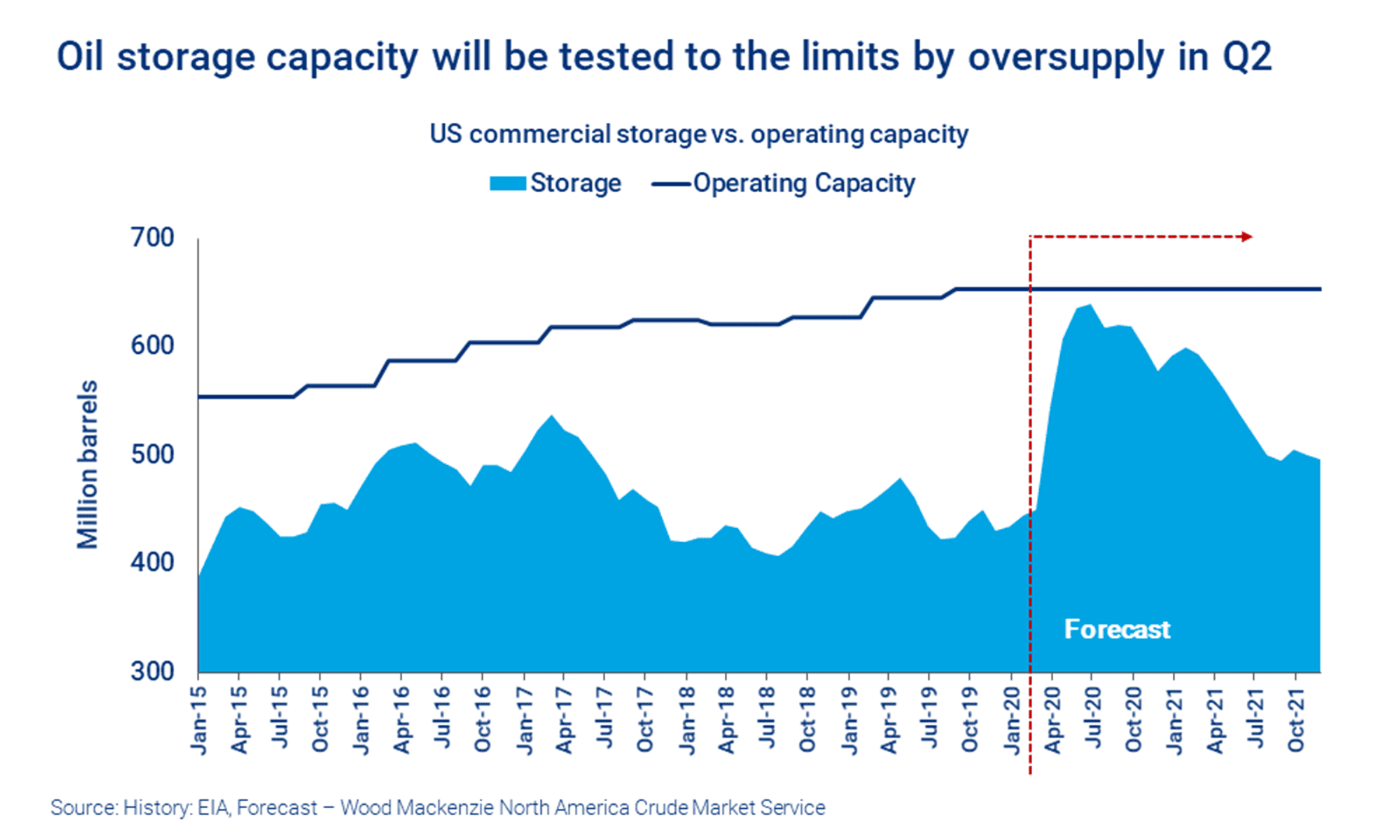

Into storage then well-head shut ins, according to WoodMac. Refiners will feel it first and cut back runs or close operations as the market for gasoline and jet fuel vanishes. Product and crude will go into storage, and when storage maxes out, including floating storage, it’s back to the well-head. Production has to be shut-in because there’s nowhere else for it to go.

WoodMac’s forecasts indicate an unprecedented oversupply of 12 million b/d for Q2. “We think there’s sufficient storage capacity in the market to absorb the oversupply for two to three months. But it depends how supply and demand play out: at times when demand is weakest, the oversupply could be much higher,” the consultancy group said.

Price will come under severe pressure, and producers will find there is no market for their crude. “We don’t think we will get to that point in the next two months or so; but if the oversupply lasts much beyond then, we’d expect to see shut-ins. It’s difficult to pinpoint geographically where production is most at risk. The constraints are not just about economics – price and SRMC – but access to local infrastructure and the market,” WoodMac said.

What’s the outlook for price?

WoodMac said this is poor in the very short term. “We expect Brent to average US$20/bbl in April and possibly, at times, to dip lower. Thereafter, much depends on how long demand is suppressed by the effects of COVID-19. We forecast demand bounces back in H2 2020, and the savage cuts in upstream investment in the last few weeks will lead to a progressively lower outlook for supply into 2021.”

A degree of market rebalancing beginning in Q3 could push Brent up towards US$40/bbl by the end of 2020. That may seem a remote possibility given today’s difficult realities, so it’s dependent on many things coming back into place, WoodMac pointed out.

Many producers today – and their financiers – would give their right arm for US$40/bbl. Yet it’s still a very modest price. Few producers, IOCs or NOCs, make any money at US$40/bbl, and there would be little or no new investment in non-OPEC supply.

COVID-19 accelerated OPEC’s strategy to an unforeseen extreme. WoodMac said once the virus retreats, the goal to win back market share can carry on, most likely at prices significantly higher than today.

{kind=link}